|

|

Tuesday, April 02 2019

CoreLogic recently released a report entitled, United States Residential Foreclosure Crisis: 10 Years Later, in which they examined the years leading up to the crisis all the way through to present day.

With a peak in 2010 when nearly 1.2 million homes were foreclosed on, over 7.7 million families lost their homes throughout the entire foreclosure crisis.

Dr. Frank Nothaft, Chief Economist for CoreLogic, had this to say,

“The country experienced a wild ride in the mortgage market between 2008 and 2012, with the foreclosure peak occurring in 2010. As we look back over 10 years of the foreclosure crisis, we cannot ignore the connection between jobs and homeownership. A healthy economy is driven by jobs coupled with consumer confidence that usually leads to homeownership.”

Since the peak, foreclosures have been steadily on the decline by nearly 100,000 per year all the way through the end of 2016, as seen in the chart below.

If this trend continues, the country will be back to 2005 levels by the end of 2017.

Bottom Line

As the economy continues to improve, and employment numbers increase, the number of completed foreclosures should continue to decrease.

Wednesday, August 22 2018

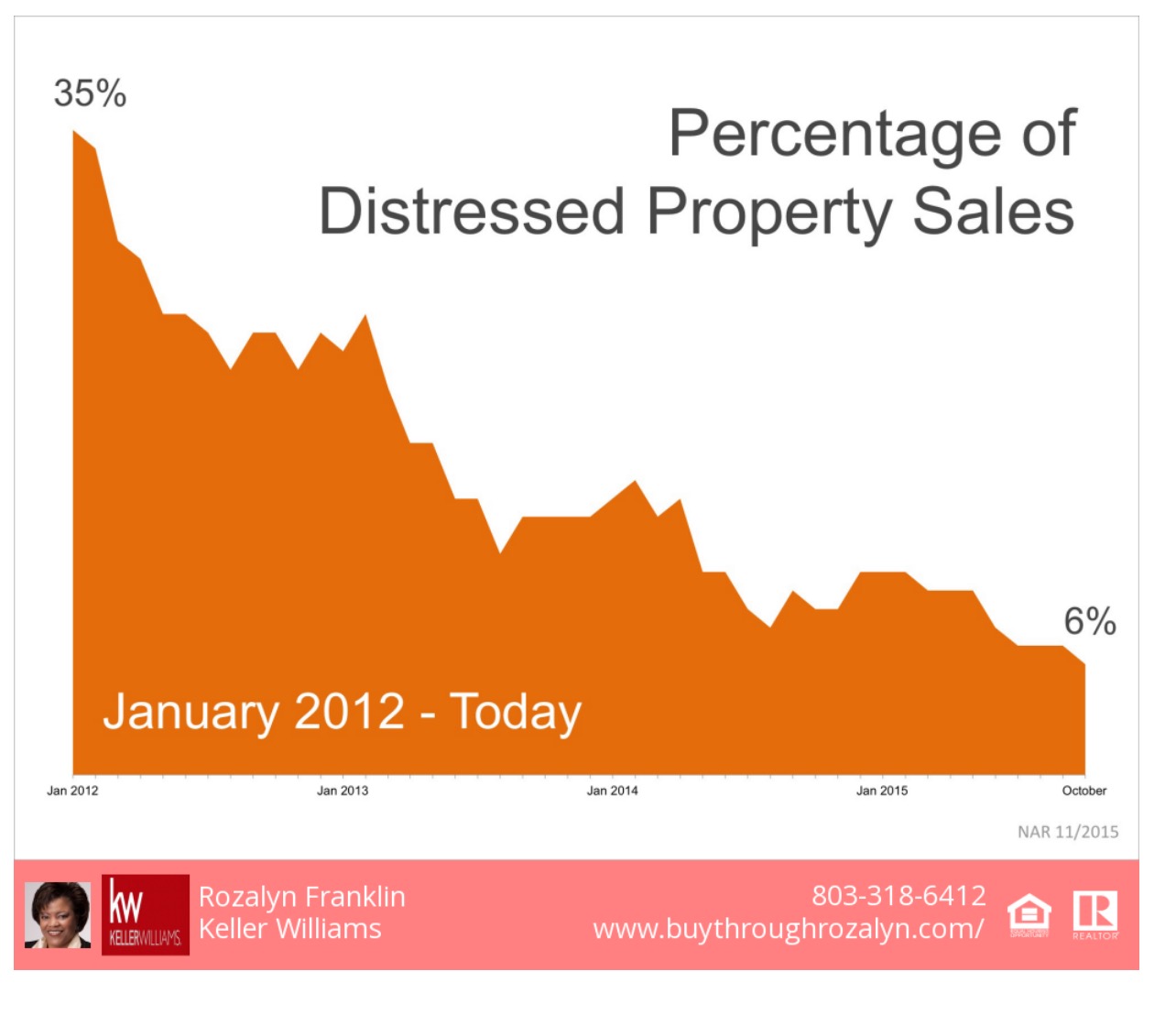

Distressed Property Sales Hit New Low

The National Association of Realtors (NAR) just released their Existing Home Sales Report revealing that distressed property sales accounted for 6% of sales in October. This is down from 9% in 2014 and the lowest figure since NAR began tracking distressed sales in October 2008.

Below is a graph that shows just how far the market has come since January 2012 when distressed sales accounted for 35% of all sales.

Existing Home Sales Up Year-Over-Year

Mortgage interest rates remained below 4% in October prompting existing home sales to stay at a healthy annual pace of 5.36 million. Year-over-year sales were up 3.9%.

Inventory of homes for sale remain below the 6-month supply that is necessary for a normal market, as they fell 2.3% to a 4.8-months supply. The shortage in inventory has contributed to the median home price rising an additional 5.8% to $219,600.

NAR’s Chief Economist, Lawrence Yun had this to say about the lack of inventory:

“New and existing-home supply has struggled to improve so far this Fall, leading to few choices for buyers and no easement of the ongoing affordability concerns still prevalent in some markets.”

There is good news though, as Yun went on to say:

As long as solid job creation continues, a gradual easing of credit standards even with moderately higher mortgage rates should support steady demand and sales continuing to rise above a year ago.”

Bottom Line:

If you are debating putting your home on the market this year, now may be the time. Buyers are still out there looking for their dream home. Let’s get together to determine your best course of action.

Wednesday, September 10 2014

Rebounding Columbia Homeowners Get Ready To Jump Back Into Home Ownership

Many Columbia homeowner who have been faced with difficulty in the pass that may have even resulted in the loss of their home. I bet we can even find that many have been on the sidelines, living in a rental apartment or in their in-laws’ spare bedroom, Patiently waiting and planning for another chance at home ownership. If this is you please know that you are not alone. I know you have been focused on rebuilding their credit, saving up for a down payment, and watching the interest rates descend to record lows while rents creep upward. Many Columbia homeowner who have been faced with difficulty in the pass that may have even resulted in the loss of their home. I bet we can even find that many have been on the sidelines, living in a rental apartment or in their in-laws’ spare bedroom, Patiently waiting and planning for another chance at home ownership. If this is you please know that you are not alone. I know you have been focused on rebuilding their credit, saving up for a down payment, and watching the interest rates descend to record lows while rents creep upward.

For those rebounding Columbia buyers eagerly waiting; Welcome to the new, always changing, confusing and often capricious world of "Mortgage Lending" It can be discouraging reading that Fannie Mae' requires a 600 FICO score, but then the lender may overlay its own requirement of a 640 FICO score,” Lender conflicts over the effect of a “unfavorable event” like a foreclosure or a Short Sale can halt an otherwise promising transaction. Don't let a Short Sale or a foreclosure dampen your enthusiasm for returning to the housing market.

Many Columbia buyers are trying to qualify for FHA loans, largely because FHA allows a 3.5 percent down payment, but to qualify the lender may require 90% LTV when attached to an " unfavorable event" requiring a much higher down payment and a waiting period of three years after a Short Sale or a foreclosure.

I have found that the biggest hurdle, even for those who have gotten their personal finances back on track, is access to the mortgage market. “Many rebounding Columbia buyers have not recuperated from long-term job loss, loss of business income, or the loss of all their savings and retirement accounts. In some cases, Columbia buyers may be ready to purchase and have the down payment money saved. They may be able to afford monthly payments. But they can’t qualify for the loan needed to make the purchase.”

This environment of fewer mortgage insurers combined with tighter restrictions on income and credit scores, “means that some rebounding Columbia Buyers with "unfavorable Events" such as a Short Sale or foreclosed may be forced to lower their home expectations and work harder to save more for the down payment.”

As a Columbia Real Estate professionals I have an obligation to help rebounding Columbia buyers understand what it takes to get back in the market. “It’s an exhausting , step-by-step process, helping a client negotiate the intricacy involved in qualifying for another loan is a job I take very seriously. If you are reaady to jump back in call me today let's talk about how I can help.

Thursday, February 13 2014

Harp 3.0 May Soon Be Here!

Originally Harp was designed to help as many as 7 million home owners, but to date it has only helped about 3 million which is far less than it was intended for. With the new Harp 3.0 availability would be open to all types of loans not just Freddie Mac and Fannie Mae; but loans such as Alt-A loans, subprime loans, and portfolio loans. I find it a little odd that subprime loans would be considered for the program, however. “So many of them were obtained with fraudulent paperwork and are laced with problems,” making me question “Why would the government want to get involved such potentially problematic loans?” They may even be discussing feature changes in HARP 3.0-example program eligibility date from May 31, 2009 to some date in 2011; offering more lenient terms on loans of 15 years or fewer; and making softer requirements for HARP investor loans.

Harp 2.0 has changed

Tuesday, December 03 2013

How To Write A Short Sale Hardship Letter

The hardship letter is one of the key factors of getting approved for a Short Sale. If you can write an accurate hardship letter and obtain a market value offer The chances of getting approval improve greatly.

Goals:

- The goal is to write a brief, yet complete, request for a lshort sale. It should be one page with no more than 3 to 4 paragraphs. They do not have time to read your life story.

- Explain why you can no longer afford your monthly house payment.

- Describe how you have tried to rectify the situation.

- Ask for help explain how you have no alternative but to seek a short sale to avoid foreclosure.

Steps:

1- In the first part of the Hardship letter, give your brief intro. Tell your lender who you are and apologize for defaulting on your obligation.

2-In the Second part, clearly explain which kind of hardship you are suffering from and what has led to the income loss. Whether you are suffering from job loss, divorce, death, business income loss or anything else. Very clearly and briefly explain your hardship. Also explain the measures you have taken to make rectify the situation (depleting your savings, borrow from family and friends, Etc.)

3-In the third or fourth if you are requesting a Short Sale ask for help. Advise that you have place the house on the market with a realtor and have no alternative but to seek a short sale to avoid foreclosure.

Tuesday, December 03 2013

Columbia SC Homeowner's new rules let you get back into homeownership sooner after foreclosure -- in theory. But will lenders play nice?

_______________________________________________________________________________________________________________

FHA and Fannie Mae are making it easier for Columbia SC homeowners who lost a home to foreclosure or short sale to buy again, but it might not make much difference if lenders don’t go along with the changes -- since they don’t have to.

First, here’s what’s new at FHA and Fannie:

FHA rules now let Columbia SC Homeowner's apply for an FHA mortgage 12 months after a foreclosure, short sale, or a deed-in-lieu of foreclosure if you meet two conditions:

1. Your loss was caused by economic conditions beyond your control. (Job Loss, Death, Illness ETC).

2. You complete housing counseling.

Note: Mortgage lenders have traditionally made Columbia SC homeowner's wait two years after a short sale or deed-in-lieu and seven years after a foreclosure to apply for a mortgage.

Once the Columbia SC homeowner has met the conditions, they will still have to meet all the usual mortgage loan rules and guidelines that lenders use for everyone -- like having enough income (and not too much debt) to afford the refinanced mortgage.

Fannie Mae credit reporting fix: Fannie, meanwhile, has cleared up a credit reporting issue that was holding back former Columbia SC homeowners who sold their homes for less than what they owed on the mortgage (a short sale) or signed over their deed to the lender to avoid foreclosure (a deed-in-lieu). Starting Nov. 16, 2013, the Fannie Mae loan underwriting system will automatically ignore the foreclosure and correctly recognize the transaction was a short sale when the code appears. Until then, Columbia SC lender's will have to manually underwrite your loan to take advantage of the change.

As always Columbia SC homeowner's need to remember that, Fannie Mae and FHA can change their own rules, but lenders don’t have to go along with the changes because the mortgage giants’ rules are simply minimum standards. Our sources say it’s likely that lenders will add their own, more restrictive rules.

Full Article

Tuesday, August 06 2013

CNNMoney Reports, Columbia home owners who are at least 90 days behind on their mortgage payments and have a Fannie Mae or Freddie Mac-backed mortgage may receive an offer from lenders to get their mortgage payments reduced.

The program will not require a delinquent Columbia home owners to file any financial paperwork. Participating Columbia homeowners will only need to make the new mortgage payments for a three-month trial period. If successful, the modification then becomes permanent.

Lenders working with the selected Columbia homeowner will reduce a monthly payment by either extending the term of the loan—or by reducing the interest rate. Columbia homeowners could see as much as a $300 difference.

To qualify for the program, Columbia home owners must have a mortgage that is at least 12 months old and they can’t be more than 24 months behind on mortgage payments. Also, the Columbia home owner’s principal balance must be 80 percent or more of the value of their home.

The program is expected to run until Aug. 1, 2015.

Source: “Thousands of borrowers to get mortgage payments reduced,” CNNMoney (July 1, 2013)

Tuesday, July 23 2013

COLUMBIA — For homeowners upside-down on their mortgage — owing more on the loan than the house is worth — foreclosure isn’t necessarily the only option

There also is a short sale.

A short sale is when a financially troubled homeowner, with the lender’s approval, sells his or her home for less than what’s owed on the loan.

Columbia homeowner's one of the main benefit of a short sale is that in many cases you may get out from under your mortgage without liability for the deficiency. A deficiency occurs when what you owe on your mortgage exceeds the amount you get when you’ve sold your home.

It is a negotiated loss to the bank between borrower and bank. “You may not even get hit with a deficiency judgment — off the hook.”

But please Columbia homeowner's don’t expect the process to be simple and effortless. Remember you are asking the lender to take a loss on your mortgage, and the financial institution won’t agree to that easily.

Gather your records: Columbia homeowners if you choose a short sale, be prepared to justify it.

Because you will be selling your home for an amount that won’t cover your loan, you can be sure your lender will want to be absolutely certain you have no other means to pay your mortgage.

“Getting out of a loan is just as hard, if not harder, than getting qualified for a loan. “They’re going to check your finances to make sure you don’t have money hidden away.”

Columbia homeowners be prepared to provide bank statements, tax returns and other documents.

“They will make sure your account is not reflecting any income coming in, “They’re going to make you prove you can’t afford it.”

Get help:

#1 Columbia homeowners need to find a real estate agent who has done short sales before.

“It’s a complex transaction that requires a lot of paperwork to go to the lender in the correct process. “If not, the short sale dies, and the consumer in most cases ends up being foreclosed on.”

The Columbia real estate agent will help you price your home so the short sale will go through.

Friday, July 12 2013

Making Homes Affordable Program Available for Columbia SC Residences

Making Home Affordable Offers Solutions

Columbia South Carolina homeowners should know the Making Home Affordable Program (MHA) ® is a critical part of the Obama Administration's broad strategy to help homeowners avoid foreclosure, stabilize the country's housing market, and improve the nation's economy.

Thousands of Columbia South Carolina homeowners have been helped by MHA programs. Columbia SC Homeowners in MHA modifications (HAMP) are typically saving more than $500 each month. And now, there are new opportunities for help. Any Columbia SC Homeowner having a tough time making their monthly mortgage payments should , Request a Modification Now!.

Columbia SC Military homeowners should check out the New! Military Resources:

Columbia SC Service members whose PCS orders have made it difficult to keep up their mortgage payments may now be eligible for mortgage help through MHA. Visit Military Resources page.

Any Columbia SC homeowner that is having a tough time making their mortgage payment should seek help, and explore all their options

Columbia SC homeowners can get free advice from a housing expert. HUD-approved housing counselors work with you and your mortgage company on your behalf, and their expertise is available for free. Call 888-995-HOPE (4673) to speak with an expert about your individual situation.

Columbia Homeowners can lower their monthly mortgage payments and get into more stable loans at today's low rates. And for those Columbia homeowners for whom homeownership is no longer affordable or desirable, the program can provide a way out that avoids foreclosure. Additionally, there are options for unemployed Columbia SC homeowners and Columbia SC homeowners who owe more than their homes are worth.

Resources from Making Home Affordable.gov Resources from Making Home Affordable.gov

Tuesday, July 09 2013

South Carolina Homeowners Beware, Bank of America is in Federal Court- Accused of routinely denying qualified borrowers a chance to modify their loans to more affordable terms.

Some Columbia Homewoners may have been lied to while working with BAnk of America loss mitigation department, while many Columbia Homeowners were delayed or stonewalled in the HAMP (loan) modification process in order for Bank of America to collect more fees, and ultimitaley upsell the borrower to a more costly in-house loan modification, charging rates 3 points higher than the 2 percent rate available under HAMP guidelines.

Columbia Foreclosure Relief

|

|

|  |

| Share This Page |

Columbia Foreclosure Relief

|

|

|